Report on the audit of the financial statements

Opinion

In our opinion:

- the financial statements of Bodycote plc (the 'parent company') and its subsidiaries (the 'group') give a true and fair view of the state of the group's and of the parent company's affairs as at 31 December 2018 and of the group's profit for the year then ended;

- the group financial statements have been properly prepared in accordance with International Financial Reporting Standards (IFRSs) as adopted by the European Union;

- the parent company financial statements have been properly prepared in accordance with United Kingdom Generally Accepted Accounting Practice, including Financial Reporting Standard 101 "Reduced Disclosure Framework" and;

- the financial statements have been prepared in accordance with the requirements of the Companies Act 2006 and, as regards the group financial statements, Article 4 of the IAS Regulation.

We have audited the financial statements which comprise:

- the Consolidated Income Statement;

- the Consolidated Statement of Comprehensive Income;

- the Consolidated and Parent Company Statements of Financial Position;

- the Consolidated Cash Flow Statement;

- the Consolidated and Parent Company Statements of Changes in Equity;

- the Group and Company Accounting Policies;

- the related notes 1 to 30 to the Group financial statements; and

- the related notes 1 to 12 to the Parent Company financial statements.

The financial reporting framework that has been applied in the preparation of the group financial statements is applicable law and IFRSs as adopted by the European Union. The financial reporting framework that has been applied in the preparation of the parent company financial statements is applicable law and United Kingdom Accounting Standards, including FRS 101 "Reduced Disclosure Framework" (United Kingdom Generally Accepted Accounting Practice).

Basis for opinion

We conducted our audit in accordance with International Standards on Auditing (UK) (ISAs (UK)) and applicable law. Our responsibilities under those standards are further described in the auditor's responsibilities for the audit of the financial statements section of our report.

We are independent of the group and the parent company in accordance with the ethical requirements that are relevant to our audit of the financial statements in the UK, including the Financial Reporting Council's (the 'FRC's') Ethical Standard as applied to listed public interest entities, and we have fulfilled our other ethical responsibilities in accordance with these requirements. We confirm that the non-audit services prohibited by the FRC's Ethical Standard were not provided to the group or the parent company.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion.

Summary of our audit approach |

| Key audit matters | The key audit matters that we identified in the current year were: - Taxation accounting – valuation of specific uncertain tax provisions

- Revenue recognition – manual adjustments to revenue

|

| Materiality | The materiality that we used for the group financial statements was £6.6 million which was determined on the basis of 5% of statutory pre-tax profit. |

| Scoping | As a consequence of the audit scope determined, we achieved coverage of approximately 74% of revenue, 75% of profit before tax and 77% of net assets |

| Significant changes in our approach | Our approach is consistent with the previous year with the exception of the removal of impairment of goodwill and intangibles and pension liability assumptions as key audit matters for the 2018 audit report. In 2018 we no longer consider the impairment of goodwill and intangible assets to be a key audit matter. This assessment is based on our risk assessment procedures and the forecast performance of the Group's cash generating units ('CGUs'). We also no longer consider the pension liability assumptions underpinning the UK defined benefit pension scheme to be a key audit matter. This follows considerations of the nature of the pension scheme and historical experience of testing of the scheme liability assumptions |

Conclusions relating to going concern, principal risks and viability statement |

| Going concern |

We have reviewed the directors' statement in the Chief Financial Officer's report to the financial statements about whether they considered it appropriate to adopt the going concern basis of accounting in preparing them and their identification of any material uncertainties to the group's and company's ability to continue to do so over a period of at least twelve months from the date of approval of the financial statements. We considered as part of our risk assessment the nature of the group, its business model and related risks including where relevant the impact of Brexit, the requirements of the applicable financial reporting framework and the system of internal control. We evaluated the directors' assessment of the group's ability to continue as a going concern, including challenging the underlying data and key assumptions used to make the assessment, and evaluated the directors' plans for future actions in relation to their going concern assessment. We are required to state whether we have anything material to add or draw attention to in relation to that statement required by Listing Rule 9.8.6R(3) and report if the statement is materially inconsistent with our knowledge obtained in the audit. | We confirm that we have nothing material to report, add or draw attention to in respect of these matters. |

| Principal risks and viability statement |

Based solely on reading the directors' statements and considering whether they were consistent with the knowledge we obtained in the course of the audit, including the knowledge obtained in the evaluation of the directors' assessment of the group's and the company's ability to continue as a going concern, we are required to state whether we have anything material to add or draw attention to in relation to: - the disclosures in the Principal risks and uncertainties that describe the principal risks and explain how they are being managed or mitigated;

- the directors' confirmation in the Directors' responsibilities statement that they have carried out a robust assessment of the principal risks facing the group, including those that would threaten its business model, future performance, solvency or liquidity; or

- the directors' explanation in the Chief Financial Officer's report as to how they have assessed the prospects of the group, over what period they have done so and why they consider that period to be appropriate, and their statement as to whether they have a reasonable expectation that the group will be able to continue in operation and meet its liabilities as they fall due over the period of their assessment, including any related disclosures drawing attention to any necessary qualifications or assumptions.

We are also required to report whether the directors' statement relating to the prospects of the group required by Listing Rule 9.8.6R(3) is materially inconsistent with our knowledge obtained in the audit. | We confirm that we have nothing material to report, add or draw attention to in respect of these matters. |

Key audit matters

Key audit matters are those matters that, in our professional judgement, were of most significance in our audit of the financial statements of the current period and include the most significant assessed risks of material misstatement (whether or not due to fraud) that we identified. These matters included those which had the greatest effect on: the overall audit strategy, the allocation of resources in the audit; and directing the efforts of the engagement team.

These matters were addressed in the context of our audit of the financial statements as a whole, and in forming our opinion thereon, and we do not provide a separate opinion on these matters.

Taxation – valuation of specific uncertain tax provisions  |

Key audit matter description

| As described in note 6 and the Group's accounting policies, the Group recognises a number of tax provisions in respect of ongoing tax inquiries and reflecting the multinational tax environment in which the Group operates. These provisions total £16.1 million (2017: £17.5 million). The tax risk concerns the judgements and estimates applied in the determination of provisions for liabilities attributed to specific uncertain tax provisions linked to the Group's corporate arrangements. This is described as an area of focus in the Report of the Audit Committee |

How the scope of our audit responded to the key audit matter

| In conjunction with our taxation audit specialists, we performed the following audit procedures in order to address this risk: - Assessed the design and implementation of the controls in place to address the key audit matter;

- Assessed the assumptions and judgements concerning the adequacy of specific uncertain tax provisions by challenging management's assumptions; and

- Reviewed the available correspondence from the various tax authorities and drawing on the experience of our taxation specialists in respect of similar situations.

|

Key observations

| From the work performed above we are satisfied that the provisions held on the balance sheet for specific uncertain tax provisions are reasonable. |

Revenue recognition - manual adjustments to revenue |

Key audit matter description

| When assessing the potential risk of fraud in relation to revenue recognition, we have considered the nature of the automated and manual transactions recorded across the Group, considering the typical sales cycle for the services provided by the Group as described in the Group's accounting policies. Following which we have determined that a key audit matter in relation to fraud exists relating to the risk of inappropriate manual adjustments being recorded in revenue. This is because the value of manual journals is material in total, and due to the risk of management override in this area. |

How the scope of our audit responded to the key audit matter

| We performed the following audit procedures in order to address this risk:

- Assessed the design and implementation of the controls in place to address the key audit matter;

- Tested the completeness and accuracy of the transactions listings split between automated and manual journal types;

- Performed procedures to understand the nature of the manual adjustments arising; and

- Selected a sample of manual entries posted throughout the year and obtained the relevant supporting documentation in order to validate that journal postings were accurate and had commercial substance.

|

Key observations

| From the work performed we have not noted any manual adjustments to revenue that we would not expect in the usual course of business, or that cannot be supported. |

Our application of materiality

We define materiality as the magnitude of misstatement in the financial statements that makes it probable that the economic decisions of a reasonably knowledgeable person would be changed or influenced. We use materiality both in planning the scope of our audit work and in evaluating the results of our work.

Based on our professional judgement, we determined materiality for the financial statements as a whole as follows:

| Group financial statements | Parent company financial statements |

|---|

| Materiality | £6.6 million (2017: £5.6 million) | £4.2 million (2017: £4.5 million) |

| Basis for determining materiality | 5% of statutory pre-tax profit (2017: 5% of expected statutory pre-tax profit) | The parent company materiality represents approximately 1% (2017: 1%) of equity. |

| Rationale for the benchmark applied | Pre-tax profit is determined to be the most stable basis of underlying business performance. | As a non-trading parent company, equity is the key driver of the company |

We agreed with the Audit Committee that we would report to the Committee all audit differences in excess of £0.33 million (2017: £0.28 million), as well as differences below that threshold that, in our view, warranted reporting on qualitative grounds. We also report to the Audit Committee on disclosure matters that we identified when assessing the overall presentation of the financial statements.

An overview of the scope of our audit

Our Group audit was scoped by obtaining an understanding of the Group and its environment, including group-wide controls, and assessing the risks of material misstatement at the Group level.

Based on this assessment, we focused our Group audit scope primarily on the audit work relating to 22 components covering the US shared service centre, the European shared service centre, UK, France and Turkey. One component within Czech Republic was removed from Group scope as part of our risk assessment process to pinpoint our focus and attention to material components where the key audit matters and judgements affecting the Group financial statements are expected. The parent company is located in the UK and audited directly by the Group audit team.

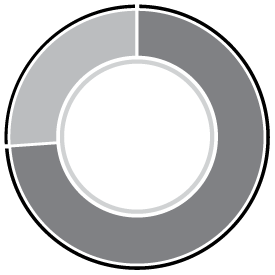

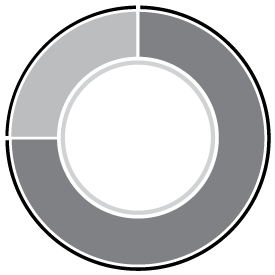

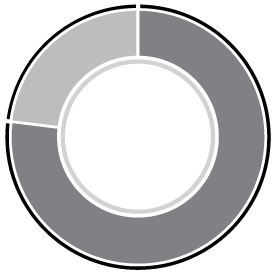

As a consequence of the audit scope determined, we achieved coverage of approximately 74% (2017: 73%) of revenue, 75% (2017: 78%) of profit before tax and 77% (2017: 79%) of net assets. Our audit work at each component was executed at levels of materiality applicable to each individual component which were lower than Group materiality. Component materiality, excluding the parent company, ranged from £1.5m to £3.0m (2017: £1.5m to £2.8m).

The Group audit team have designed the audit procedures for all significant risks to be addressed by the component auditors and issued Group referral instructions detailing the nature and form of the reporting required. The Group audit team continued to follow a program of planned visits that has been designed so that a senior member of the Group audit team visits each of the significant finance function locations included as full scope for the Group audit on a rotational basis. During the year, senior members of the Group audit team have visited the US shared service centre, the European shared service centre, and France.

In years when we do not visit a material component we include the component audit team in our team briefing, discuss their risk assessment, attend close meetings by conference call and review documentation of the findings from their work.

At the parent entity level we also tested the consolidation process and carried out analytical procedures to confirm our conclusion that there were no significant risks of material misstatement of the aggregated financial information of the remaining components not subject to audit or audit of specified account balances.

Revenue

- Full audit scope 74%

- Review at Group level 26%

Profit before tax

- Full audit scope 78%

- Review at Group level 22%

Net assets

- Full audit scope 79%

- Review at Group level 21%

Other information |

|---|

The directors are responsible for the other information. The other information comprises the information included in the annual report, other than the financial statements and our auditor's report thereon. Our opinion on the financial statements does not cover the other information and, except to the extent otherwise explicitly stated in our report, we do not express any form of assurance conclusion thereon. In connection with our audit of the financial statements, our responsibility is to read the other information and, in doing so, consider whether the other information is materially inconsistent with the financial statements or our knowledge obtained in the audit or otherwise appears to be materially misstated. If we identify such material inconsistencies or apparent material misstatements, we are required to determine whether there is a material misstatement in the financial statements or a material misstatement of the other information. If, based on the work we have performed, we conclude that there is a material misstatement of this other information, we are required to report that fact. In this context, matters that we are specifically required to report to you as uncorrected material misstatements of the other information include where we conclude that: - Fair, balanced and understandable – the statement given by the directors that they consider the annual report and financial statements taken as a whole is fair, balanced and understandable and provides the information necessary for shareholders to assess the group's position and performance, business model and strategy, is materially inconsistent with our knowledge obtained in the audit; or

- Audit committee reporting – the section describing the work of the audit committee does not appropriately address matters communicated by us to the audit committee; or

- Directors' statement of compliance with the UK Corporate Governance Code – the parts of the directors' statement required under the Listing Rules relating to the company's compliance with the UK Corporate Governance Code containing provisions specified for review by the auditor in accordance with Listing Rule 9.8.10R(2) do not properly disclose a departure from a relevant provision of the UK Corporate Governance Code.

| We have nothing to report in respect of these matters. |

Responsibilities of directors

As explained more fully in the directors' responsibilities statement, the directors are responsible for the preparation of the financial statements and for being satisfied that they give a true and fair view, and for such internal control as the directors determine is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

In preparing the financial statements, the directors are responsible for assessing the group's and the parent company's ability to continue as a going concern, disclosing as applicable, matters related to going concern and using the going concern basis of accounting unless the directors either intend to liquidate the group or the parent company or to cease operations, or have no realistic alternative but to do so.

Auditor's responsibilities for the audit of the financial statements

Our objectives are to obtain reasonable assurance about whether the financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditor's report that includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with ISAs (UK) will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these financial statements.

Details of the extent to which the audit was considered capable of detecting irregularities, including fraud are set out below.

A further description of our responsibilities for the audit of the financial statements is located on the FRC's website at: www.frc.org.uk/auditorsresponsibilities. This description forms part of our auditor's report.

Extent to which the audit was considered capable of detecting irregularities, including fraud

We identify and assess the risks of material misstatement of the financial statements, whether due to fraud or error, and then design and perform audit procedures responsive to those risks, including obtaining audit evidence that is sufficient and appropriate to provide a basis for our opinion.

Identifying and assessing potential risks related to irregularities

In identifying and assessing risks of material misstatement in respect of irregularities, including fraud and non-compliance with laws and regulations, our procedures included the following:

- enquiring of management, internal audit and the audit committee, including obtaining and reviewing supporting documentation, concerning the group's policies and procedures relating to:

- identifying, evaluating and complying with laws and regulations and whether they were aware of any instances of non-compliance;

- detecting and responding to the risks of fraud and whether they have knowledge of any actual, suspected or alleged fraud;

- the internal controls established to mitigate risks related to fraud or non-compliance with laws and regulations;

- discussing among the engagement team, including material component audit teams, and involving relevant internal specialists, including tax, valuations, pensions and IT, specialists regarding how and where fraud might occur in the financial statements and any potential indicators of fraud; and

- obtaining an understanding of the legal and regulatory frameworks that the group operates in, focusing on those laws and regulations that had a direct effect on the financial statements or that had a fundamental effect on the operations of the group. The key laws and regulations we considered in this context included the UK Companies Act, Listing Rules, pensions and tax legislation.

Audit response to risks identified

As a result of performing the above, we identified manual adjustments to revenue and valuation of specific uncertain tax provisions as key audit matters. The key audit matters section of our report explains the matters in more detail and also describes the specific procedures we performed in response to those key audit matters.

In addition to the above, our procedures to respond to risks identified included the following:

- reviewing the financial statement disclosures and testing to supporting documentation to assess compliance with relevant laws and regulations discussed above;

- enquiring of management, the audit committee and in-house / external legal counsel concerning actual and potential litigation and claims;

- performing analytical procedures to identify any unusual or unexpected relationships that may indicate risks of material misstatement due to fraud;

- reading minutes of meetings of those charged with governance, reviewing internal audit reports and reviewing correspondence with HMRC; and

- in addressing the risk of fraud through management override of controls, testing the appropriateness of journal entries and other adjustments; assessing whether the judgements made in making accounting estimates are indicative of a potential bias; and evaluating the business rationale of any significant transactions that are unusual or outside the normal course of business.

We also communicated relevant identified laws and regulations and potential fraud risks to all engagement team members including internal specialists, and remained alert to any indications of fraud or non-compliance with laws and regulations throughout the audit.

Report on other legal and regulatory requirements

Opinions on other matters prescribed by the Companies Act 2006

In our opinion the part of the directors' remuneration report to be audited has been properly prepared in accordance with the Companies Act 2006.

In our opinion, based on the work undertaken in the course of the audit:

- the information given in the strategic report and the directors' report for the financial year for which the financial statements are prepared is consistent with the financial statements; and

- the strategic report and the directors' report have been prepared in accordance with applicable legal requirements

In the light of the knowledge and understanding of the group and of the parent company and their environment obtained in the course of the audit, we have not identified any material misstatements in the strategic report or the directors' report.

Matters on which we are required to report by exception |

|---|

| Adequacy of explanations received and accounting records |

Under the Companies Act 2006 we are required to report to you if, in our opinion: - we have not received all the information and explanations we require for our audit; or

- adequate accounting records have not been kept by the parent company, or returns adequate for our audit have not been received from branches not visited by us; or

- The parent company financial statements are not in agreement with the accounting records and returns.

| We have nothing to report in respect of these matters. |

| Directors' remuneration |

Under the Companies Act 2006 we are also required to report if in our opinion certain disclosures of directors' remuneration have not been made or the part of the directors' remuneration report to be audited is not in agreement with the accounting records and returns. | We have nothing to report in respect of these matters. |

Other matters

Auditor tenure

Following the recommendation of the audit committee, we were appointed by the Board of Directors in 2002 to audit the financial statements for the year ending 31 December 2003 and subsequent financial periods. The period of total uninterrupted engagement including previous renewals and reappointments of the firm is 16 years, covering the years ending 31 December 2003 to 31 December 2018.

Consistency of the audit report with the additional report to the audit committee

Our audit opinion is consistent with the additional report to the audit committee we are required to provide in accordance with ISAs (UK).

Use of our report

This report is made solely to the company's members, as a body, in accordance with Chapter 3 of Part 16 of the Companies Act 2006. Our audit work has been undertaken so that we might state to the company's members those matters we are required to state to them in an auditor's report and for no other purpose. To the fullest extent permitted by law, we do not accept or assume responsibility to anyone other than the company and the company's members as a body, for our audit work, for this report, or for the opinions we have formed.

Mark Mullins, FCA (Senior statutory auditor)

for and on behalf of Deloitte LLP

Statutory Auditor

London, United Kingdom

8 March 2019